There’s a bill currently in Parliament that’s aiming to make the rules clearer when it comes to contractors and employees in New Zealand. So if you’re not 100% sure whether someone is truly a contractor or an employee, now’s the time to get clear. Because once the rules tighten, mistakes could get expensive, whether you’re paying contractors or are one.

Whether you’re using contractors in your business or are one yourself, we’ve written a blog that breaks it down in plain English. You’ll learn what’s being clarified, what to look out for, and what we recommend to keep things simple and safe for everyone involved.

Are You Employing Contractors or Setting Yourself Up for Trouble?

The difference between a contractor and an employee has been confusing for years. Now the government is stepping in to help tidy things up. The Employment Relations Amendment Bill has been introduced to Parliament. It’s not law yet, but it’s designed to clarify the difference between a contractor and an employee, and it’s expected to impact a wide range of industries.

A lot of the recent focus has been on the gig or side-hustle economy; roles like Uber drivers or self-employed owner-drivers contracted to NZ Post. These workers have often been treated as contractors but expected to behave like employees. That’s where the contractor versus employee line gets blurry, and where it’s easy for businesses to get caught out.

If you’re a business owner using contractors, now’s the time to ask: are they genuinely independent, or does the relationship look more like employment?

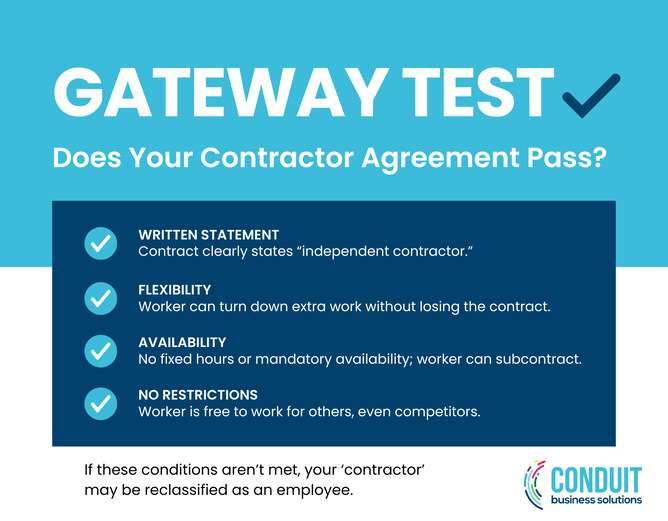

The Gateway Test

The Gateway Test in the new bill sets a minimum standard for contractor agreements. To be accepted, the contract must be in writing and clearly state the worker is an independent contractor. But that’s not enough. The worker also has to have real independence. That means they can turn down extra tasks without losing the contract, they don’t have to be available at fixed times or hours, they can subcontract the work, and they’re free to work for other businesses (including competitors). If these conditions aren’t met, the agreement may not pass the Gateway Test and the person could be treated as an employee.

Do You Need a Contractor Agreement?

In New Zealand, a contractor agreement isn’t legally required by Inland Revenue (IRD) or MBIE, but it’s strongly advised.

Here’s why:

Not legally required

IRD doesn’t use contracts to decide tax treatment. Instead, contractors must either give the payer a completed IR330C Tax Rate Notification for Contractors form (showing their chosen tax rate) or provide a valid Certificate of Exemption (IR332) if no tax is to be deducted.

MBIE and the Employment Relations Authority look at the real nature of the relationship. Even with a contract, if someone is treated like an employee, they may still be deemed an employee.

Strongly advised

Having a clear contractor agreement is recommended because it:

Defines the relationship. Confirms it’s an independent contractor arrangement, not employment.

Sets expectations. Scope of work, payment terms, invoicing, use of tools/equipment, confidentiality and health and safety responsibilities.

Manages risk. Helps show you’ve taken reasonable steps to treat them as a contractor, not an employee.

Supports compliance. Useful evidence if MBIE, IRD, or the ERA review the arrangement.

Avoids disputes. Clear terms reduce the risk of misunderstandings over pay, hours, or responsibilities.

Practical tip

For businesses (payers): always have a written contractor agreement signed by both parties. A signed agreement confirms the terms, reduces disputes, and provides evidence if MBIE, IRD, or the ERA review the relationship.

If you’re working with Building subcontractors, this free contractor agreement template NZ from Tradify can help keep things tidy and clear:

🔗 Get the free building subcontractor agreement template from Tradify

For contractors: keep a signed agreement on file. It shows professionalism, helps prove you’re genuinely self-employed, and protects you if expectations aren’t met.

In short: a signed contractor agreement isn’t compulsory, but it protects both sides and helps avoid miscommunication.

What the New Bill Changes

Even under the new bill, MBIE and the Employment Relations Authority will still look at the real nature of the relationship. A contract on its own isn’t enough, if someone is treated like an employee, they may still be deemed one. What’s changing is the addition of a new Gateway Test, which gives more weight to a proper contractor agreement. If the contract makes it clear the person has genuine flexibility (no fixed hours, can subcontract work, can turn down tasks, and can work for others), it’s more likely to be accepted that they’re a contractor. In short: contracts matter more under the new bill, but they only work if the reality of the working relationship matches what’s written down.

Why It’s Often Better to Let Contractors Handle Their Own Withholding Tax

For most genuine contractors, it makes more sense to keep tax responsibility with them rather than the payer.

For the Payer (business/principal):

Less admin. No calculating, filing, or paying withholding tax.

Cleaner accounts. Pay the full invoice, claim GST if applicable, no messy reconciliations.

Lower risk. Mistakes with withholding tax attract harsh IRD penalties.

Cost savings. No need for payroll software just to process contractors.

For the Contractor:

You control your own income tax and cash flow.

You know what’s been paid and what’s still owing.

You choose the right tax rate for your industry on the back of the IR330C Tax rate notification for contractors form or apply for a Certificate of Exemption (IR332).

Contractors outside these industries can choose to have their income treated as Voluntary schedular payments by agreement with the payer (you still use an IR330C to set the rate).

Shows you’re operating as a legitimate business.

What Each Party Must Do

For the Payer (business/principal):

Check if schedular payments apply for your industry (construction, agriculture, labour hire, entertainers, directors, etc.).

Get an IR330C from every contractor and deduct tax at their chosen rate (10–33%).

No IR330C? Deduct at 45% (20% for non-resident companies).

Apply tailored or prescribed rates if IRD issues a certificate.

Keep certificates of exemption (IR332) on file and check they’re current.

File and pay withholding tax in your employer returns on time.

For the Contractor:

Complete your IR330C and give it to the payer. No form = 45% deductions.

Choose wisely, apply for a tailored tax rate if needed (minimum 10%).

Exemption option, apply for an IR332 Certificate of Exemption if eligible.

Prescribed rates, if you have tax debt, IRD may set one and you must supply it to the payer.

GST, register if earning $60k+ per year, and charge GST on invoices if registered.

Stay responsible, even if tax is withheld, you must file returns, keep records, and pay any other tax due.

Final Word

This isn’t just about ticking compliance boxes. It’s about getting clear on roles, responsibilities, and risk. Whether you’re hiring contractors or working as one, now’s the time to make sure everything stacks up.

This bill is all about clearing up the confusion, but once that clarity becomes law, there’ll be less room for mistakes.

Got questions about contractors, employees, withholding tax, or just want to make sure you’re on the right track?

Book a free discovery meeting and we’ll talk through your setup, your obligations, and the smartest way forward.